The question every anesthesia provider wants to answer is whether the billing staff is collecting everything that is collectable for the valuable services provided. Predicting the expected value of all the service provided by an anesthesia practice is not such an easy task that requires a detailed understanding of the services provided and payor guidelines for each. While there are many ways to evaluate performance, most are shortcuts that don’t provide accurate results. Anyone who says anesthesia billing is easy is either a terrible biller or a terrible liar. Anesthesia billing is unlike that of any medical specialty. The calculation of anesthesia charges an arcane discipline that requires a careful review of each anesthesia record to determine the billable services. Many payers have their own specific rules for calculation allowable payments. The challenge is that the billing staff must capture a number of details for each case so that they have what they need to prepare a specific payer claim. The reason so many anesthesia practices outsource their billing is that billing is simply too complicated to perform consistently without a qualified team of experts. As is true of any service relationship, the client must understand the complexity of the task to appreciate the accuracy of the results.

The irony is that while anesthesia providers have a powerful armamentarium of monitors to evaluate the appropriateness and effectiveness of their anesthesia technique, they lack the necessary tools to know exactly how well the billing process is being managed because the adjudication of claims is somewhat of a black box. This is why the relationship between the provider and the billing staff is always based on a high degree of trust. While monthly management reports provide a considerable amount of data with regard to production trends, collections and key performance metrics, such as days in AR (DAR) and the percentage of AR over 90 days, such metrics don’t reflect unique idiosyncrasies of anesthesia billing.

SURGICAL ANESTHESIA CHARGES AND PAYMENTS

Billing for anesthesia services requires identifying three types of charges: time based surgical anesthesia (85 percent), obstetric anesthesia (13 percent) and non-time-based procedural services (3 percent), each of which has its own rules and conventions. It is these distinctions that make anesthesia billing unique. Failure to track each of these component parts will result in an incomplete understanding of the practice. The key to effective billing is to be able to predict the expected value of each month’s services. If the volume of services declines or if there are payer processing problems the billing staff should be able to predict the extent of the impact.

The majority of anesthesia charges and payments are calculated based on a tally of base and time units, typically based on a 15-minute unit. The total billable units are calculated for each case and then multiplied by a practice conversion factor, or charge per unit, to determine the total charge and them by a payer conversion factor to determine the allowable payment by each payer. One might assume that this makes it easy to determine whether the payment is for a given case, but it is not that simple. Actual payments are adjusted by a variety of factors including copayment and deductible. The net collection percentage measures the disparity between the expected payment and the actual payment. Most management reports include a net collection percentage, but it is only valid if it only refers to surgical payments.

How do you know what you should be collecting per surgical unit? The key is payer mix. Knowing what percentage of billable surgical units are billed to each insurance plan is the key to revenue potential. Payers can be grouped into three broad categories: public payers (Medicare and Medicaid), commercial payers and self-pay. Since public payment rates are set by the government they tend to be significantly discounted, which draws the overall average down. Commercial rates may be meaningful, which helps raise the average rate. Obviously, patients with no insurance have a very limited ability to pay.

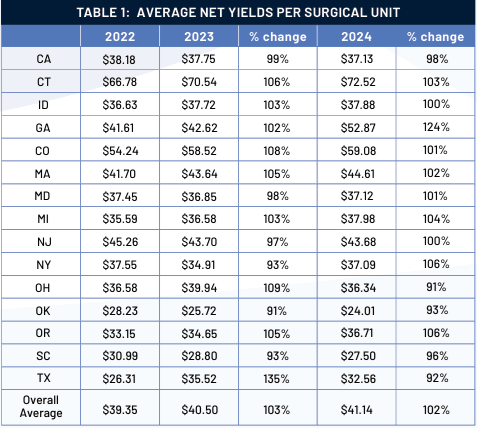

Table 1 indicates a sample of Coronis Health practices from across the country for a period of three years. Rates are very reflective of the payer mix.

This table demonstrates three key aspects of reference data. As discussed above, payer mix has a significant impact on the rate for each practice. The good news is that despite Medicare rates remaining basically flat, the overall averages have been trending up by two to three percent per year. The bad news is that the rate of increase is decreasing. Eventually rates will probably start to decrease.

Projecting the expected value of each month’s surgical activity involves two variables, the number of billed units and the projected yield per billed unit, which is typically total actual date of service collections for an extended period of time divided by billed surgical units for the same timeframe. Best results are obtained if this calculation is based on a six-month lag.

OBSTETRIC ANESTHESIA CHARGES AND PAYMENTS

Why is it essential to separate obstetric anesthesia performance? Obstetric anesthesia charges are calculated based on a modified surgical formula. Base values are not based on the complexity of the case, per se, but on the mode of anesthesia and the outcome of the delivery. Time units may be calculated on a variety of conventions depending on the preference of the practice. The notion of a 15-minute unit does not reflect billable obstetric anesthesia time. One common method for calculating OB anesthesia time, for example, assigns two or three units for the setting of the epidural and one or two units per hour of epidural monitoring. Some Medicaid programs even require documentation of the precise attendance of the provider to the epidural. With regard to payment for OB anesthesia services, major payers tend to have unique criteria. Most will recognize ASA base values but limit the number of payable units.

Because of this the accuracy of OB payments must be based on the specific rules for each payer. Trying to calculate the average yield per unit billed does not tell one much. A much more useful reference metric is the yield per case. The best way to predict obstetric revenue potential is to multiply the average yield per case by the number of cases.

FLAT FEE PROCEDURE CHARGES AND COLLECTIONS

Revenue for non-time-based procedures such as invasive monitoring, nerve blocks and evaluation and management services (E&M services) never represents a large percentage of total revenue, but such procedures are nevertheless important to monitor because these may represent revenue opportunities. Charges for invasive monitoring, arterial lines, CVPs, Swan-Ganz catheters and TEE are for CABGs and cardiovascular cases. It is important to ensure that these are being captured. Charges for nerve blocks represent a significant adjunct to anesthesia for orthopedic cases. For many practices these represent one of the fastest growing sources of additional revenue.

The point is that these charges are all based on flat fees and are paid from fee schedules established by each payer. While the ASA assigns base values to all of these procedures it is important to note that these units cannot be evaluated as similar to surgical units because the allowable payments are not based on ASA units. What most practices are concerned about is whether all these procedures are actually being paid.

What is the point of all this? Reliable performance assessment involves the ability to determine the expected revenue potential of each aspect of the practice so that one can measure what percentage of the expected in being collected based on the ability to post payments against the charges that they are paying off, a methodology referred to as date of service (DOS). Optimal results should be at least 95 percent. Anesthesia providers should use these guidelines as a template for evaluating their performance.

Many anesthesia providers have a tendency to believe that the purpose of the billing staff is to ensure that they will optimize the collections for the valuable services they perform. While it is true that qualified billing staff is critical to the effective management of accounts receivable, effective billing is a partnership. Providers must know how to document the services completely and in compliance with all current guidelines and requirements. They must also know when there are questions or problems that require their prompt attention. Just as they must always know how their patients are responding to the drugs and agents they are administering; they must also know and appreciate the challenges the billing staff is experiencing. This is why a detailed understanding of the arcane nature of anesthesia billing is so critical to the optimal results they desire.

Jody Locke, MA serves as vice president of anesthesia and pain practice management services for Coronis Health. Mr. Locke is responsible for the scope and focus of services provided to Coronis Health’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He is a key executive contact for groups that enter into contracts with Coronis Health. Mr. Locke can be reached at jody.locke@coronishealth.com.